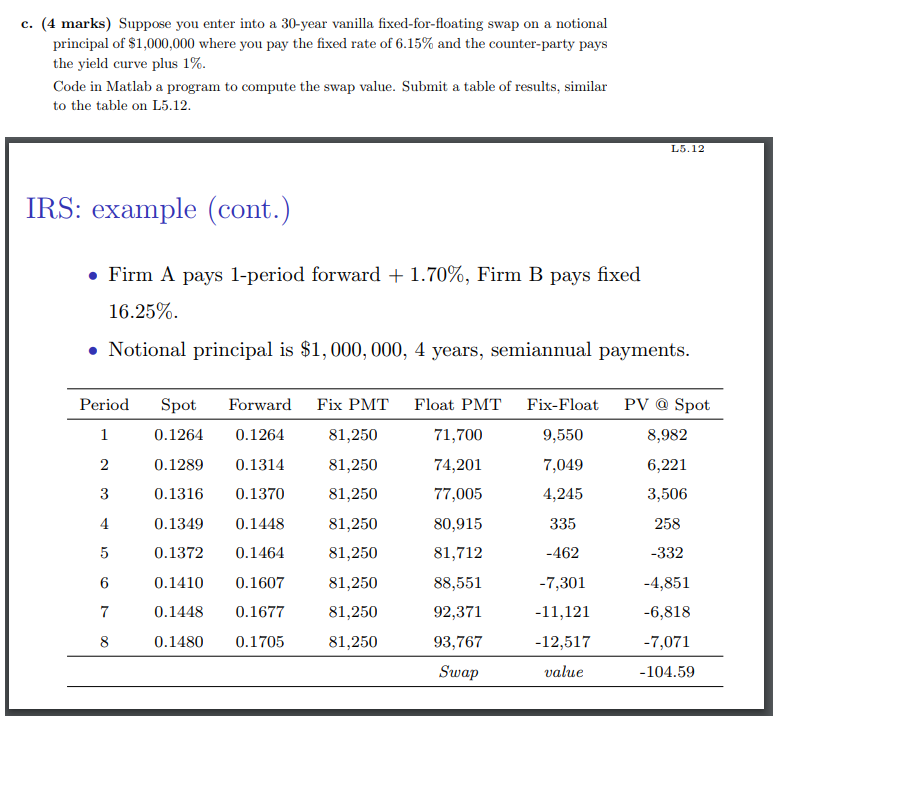

c. (4 marks) Suppose you enter into a 30-year vanilla fixed-for-floating swap on a notional principal of $1.000.000 where you pay the fixed rate of 6.15% and the counter-party pays the yield curve plus 1%. Code in Matlab a program to compute the swap value. Submit a table of results, similar to the table on L5.1:2 L5.12 IRS: example (cont.) . Firm A pays 1-period forward + 1.70%, Firm B pays fixed 16.25% Notional principal is $1,000,

OR

PayPal Gateway not configured

OR

PayPal Gateway not configured